Showing posts with label MORTGAGE FORECLOSURES. Show all posts

Showing posts with label MORTGAGE FORECLOSURES. Show all posts

Tuesday, March 22, 2011

Sunday, September 26, 2010

Wealth inequality rivals the months prior to the Great Depression

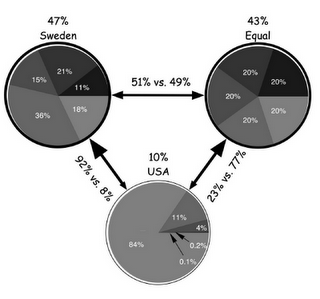

The official announcement that the recession is over underscores the massive disconnect between Wall Street and the rest of America. Wealth inequality in America is at levels last seen right before the Great Depression ravaged our economy. Yet the inequality has grown even more intense as this crisis has gone forward. 43 million Americans are now classified as being in poverty. This trend hasn’t shifted in the last decade, recession or no recession. The system is absolutely flawed and that is why we have over 16 percent underemployment, 41 million Americans on food stamps, 4 out of 10 workers in low paying service sector jobs, the median household income falling under $50,000, record monthly foreclosure filings, and yet the recession is over according to a small group of economists. The recession may be over for Wall Street but the rest of America is still struggling.

Wealth inequality has been exacerbated by the casino like behavior of investment banks on Wall Street. A recent study shows how out of touch with the facts most Americans are when it comes to wealth inequality in their own country. One fascinating finding is that most Americans, even between those that make $50,000 and $100,000 actually envision optimal wealth distributions that are very similar:

Read Full Article

Fresh food that lasts from eFoods Direct (Ad)

Live Superfoods

Print this page

Thursday, September 16, 2010

Foreclosures Rise; Repossessions Set Record

Joseph Pisani

Bank repossessions, often the final step in the foreclosure process after a home fails to sell at auction, increased about 2 percent from the month before to 95,364, a record high. At the same the number of properties that received default notices—the first step in the foreclosure process—decreased 1 percent from a month ago and fell 30 percent from a year ago, a sign that lenders are focusing on their backlog of foreclosure inventory before tackling new distressed loans, according to foreclosure listing website RealtyTrac, which released the report.

Read Full Article

Fresh food that lasts from eFoods Direct (Ad)

Live Superfoods

Save the Banks and Kill the Economy

By Prof Rodrigue Tremblay | |

Global Research, September 12, 2010 | |

It has become a truism to say that the Democrats and the Obama administration now “own” the crucial issue of the economy. Justly or unjustly, voters are bound to hold them accountable for the poor state of the U.S. economy. This is not an enviable political position to be in just before an election, at a time when disgusted voters are most angry and very anxious about the economy and their economic future. Recent polls indicate that nearly two-thirds of Americans think their nation is in a state of decline and that the economy will remain in the same recessionary state or get worse next year. Contrary to what President Franklin D. Roosevelt did in the 1930s, President Barack Obama did not confront the banking industry head-on after fraudulent practices caused one of the worst financial crises in U.S. history. In particular, he did not reverse the blanket financial deregulation that the Clinton and Bush administrations engineered in 1999, in 2000, in 2004, in 2005 and in 2007 that allowed for creating mortgage-linked synthetic subprime securities and for betting against them. Instead, his economic operatives (Geithner, Summers, Bernanke, Orszag, Emanuel, (L.A.) Sachs, Romer, Bair, ...etc.) threw trillions of public dollars to the largest banks, allowing top bankers to keep enjoying hundreds of million of dollars in yearly bonuses, at a time when some 300,000 Americans are losing their homes throughforeclosures every month. Such a persistent epidemic of home foreclosures is creating a tremendous drag on the economy, besides being a social disaster. —The system that is responsible for so many home foreclosures has not been fixed, although valiant attemptshave been made to mitigate the process. Meanwhile, also with the intention of saving the largest banks, regulators began pressing the banks to raise capital asset ratios and to shrink their risk assets. The Bernanke Fed went so far as to lend money to the largest banks at zero interest rate, while paying interest on the excess reserves the banks kept at the Fed, a practice that resulted in an outright gift to the banks. All these policies have resulted in tightening credit availability and in provoking the largest plunge in the M3 money supply since the Great Depression. As long as this condition endures, there won't be any substantial economic recovery in the United States. Just as Obama did for the wars, when he kept in position and even promoted Bush operatives Gates and Petraeus, Obama kept or brought back as his economic team some of the very Wall Street-connected people who were responsible for creating the conditions that led to the financial crisis in the first place. Now, at mid-term, President Barack Obama is saddled with the devastating image of a defender and promoter of Bush's wars in Afghanistan and Iraq and is viewed by many as having sided with Wall Street bankers against Main Street folks, just as George W. Bush did with his Goldman Sachs-connected Treasury Secretary Henry Paulson and his banking bailouts. To many Americans, indeed, the Obama administration looks more and more like a third-term Bush II administration. For many Americans, it's a nightmare. The biggest mistake that President Barack Obama seems to have made, at the beginning of his mandate, was to not disassociate himself more clearly from the previous Bush administration. Now, it's too late, and unfortunately for him and the divided Democrats, they are poised to suffer the wrath of an enraged and disillusioned electorate. Indeed, with U.S. real unemployment rate hovering around 17 percent, with 3 out of 4 workers telling pollsters that they doubt that their wages will increase next year, with many American households' financial situation deteriorating, with home foreclosures approaching 10 million, with huge fiscal deficits and future tax hikes likely, with the Bernanke Fed adopting third-world monetary policies in monetizing the public debt, and with an overall anemic economic growth, the Obama administration and the Democratic Congress are going into the November 2 midterm elections with many monkeys on their backs and very little public confidence. The only thing that runs in their favor is the poor quality and vision of their Republican opponents who have followed an obstructionist strategy and have sided time and again with lobbyists, thus blocking most attempts to straighten things up. Only a credible campaign to persuade the electorate in extremis that Democrat incumbents are “less worse” than their Republican opponents, coupled with a high turnout at the polls could prevent a Democratic bloodbath in the U.S. Congress, especially in the House of Representatives, next November. —If not, President Barack Obama will officially become a lame-duck president after November 2, and Congress will be paralyzed at a very crucial time when strong leadership is required to get out of the economic mess. This is a most unappealing perspective. Rodrigue Tremblay is professor emeritus of economics at the University of Montreal and can be reached at rodrigue.tremblay@yahoo.com . He is the author of the book "The Code for Global Ethics | |

Please support Global Research Global Research relies on the financial support of its readers. Your endorsement is greatly appreciated | |

| Subscribe to the Global Research e-newsletter | |

Disclaimer: The views expressed in this article are the sole responsibility of the author and do not necessarily reflect those of the Centre for Research on Globalization. The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible or liable for any inaccurate or incorrect statements contained in this article. To become a Member of Global Research The CRG grants permission to cross-post original Global Research articles on community internet sites as long as the text & title are not modified. The source and the author's copyright must be displayed. For publication of Global Research articles in print or other forms including commercial internet sites, contact: crgeditor@yahoo.com www.globalresearch.ca contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of "fair use" in an effort to advance a better understanding of political, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than "fair use" you must request permission from the copyright owner. For media inquiries: crgeditor@yahoo.com © Copyright Rodrigue Tremblay, Global Research, 2010 The url address of this article is: www.globalresearch.ca/index. | |

© Copyright 2005-2007 GlobalResearch.ca Web site engine by Polygraphx Multimedia © Copyright 2005-2007 | |

Live Superfoods

Sunday, September 5, 2010

5 Doomsday Scenarios for the U.S. Economy

Comment: I am seldom amazed at how the writers at The Atlantic always seem to leave out any mention of the Central Banking Cartel and the Federal Reserve in their version of the Economic Crisis; choosing, instead, to suggest that the American consumer is one possible cause of an economic collapse

.

By Derek Thompson and Daniel Indiviglio

The Atlantic

It's been a brutal summer for the economy. The housing sector, like a balloon batted in the air one last time by the government credit, resumed its inevitable fall. Economic growth slowed to a lead-footed 1.6 percent, and job growth is even more anemic. Meanwhile, consumers arecranky, the trade gap is gaping.

Most signs point to a slow and steady recovery, but what if the pessimists are right, again? What if the United States isn't in the slow-lane to recovery, but rather on the precipice of another decline -- a double dip?

To see where this re-recession might begin, my colleague Dan Indiviglio and I imagined five financial earthquakes, each with a single epicenter: housing, consumers, toxic assets, Europe, and the debt. The following five scenarios are listed in order of likelihood.

1. Housing's Mini-Bubble Pops

1. Housing's Mini-Bubble Pops

Perhaps nothing poses as a big of a concern to the U.S. economy as its housing market. It's unclear how the government's efforts to stabilize the market through a buyer credit, ultra-low mortgage rates, and mortgage modification programs will pan out. Did it just create another mini-bubble that's beginning to pop now that the support has been withdrawn?

Here's the scenario. Weak home sales and continuing foreclosures result in climbing real estate inventory. This has two effects. First, it makes new homes even less attractive which furtherreduces construction jobs. Second, it puts downward pressure on home prices, which makes it harder for struggling homeowners to sell their home to avoid foreclosure and also keeps strategic default rates high, exacerbating the problem. Lower home values encourage Americans to save more and spend less, since their wealth is effectively reduced. The Dow drops and credit markets tighten even further, suffocating private investment just as homeowners bunker down and slash spending. Growth turns negative.

2. You Break the Economy

2. You Break the Economy

You, the American consumer, are reloading savings after a debt-fueled decade. But as any general will tell you, when an entire squad reloads at once, it leaves everybody vulnerable. It's the same with the economy.

Here's the scenario. Consumer sentiment continues to fall slowly, and spending turns negative again. Small businesses hold off to replenish their inventories or add new workers. Wages and hours freeze, and unemployment takes a leap toward 10 percent in October. Congress is paralyzed, because it's only weeks away from the mid-terms. The stock market sees business revenue trending flat, joblessness rising and Congress doing nothing, and it sparks a 300-point sell-off. Americans frightful for their savings cut back spending even more the next month, and overall growth turns negative.

3. Toxic Assets Return

3. Toxic Assets Return

If you closely followed the bank bailout, then you know it wasn't originally billed as simply throwing money at the banks. Instead, the Treasury intended to purchase the toxic assets from banks, which were the source of investors' uncertainty concerning bank stability. But the Treasury couldn't figure out a way to do this quickly enough to make it effective. As a result, the banks were largely stuck with these bad assets. We just don't know how bad, yet.

Here's the scenario. The residential real estate market's problems continue. Even once foreclosures begin to decline, we see waves of defaults, as modification program participants re-default at rates of 30% to 50%. Commercial mortgage-backed securities continue to deteriorate, as some businesses struggle with weak consumer demand. Home and commercial real estate values keep declining, and so do the value of the assets that back them. Banks with exposure to these toxic securities see another round of losses, and investors question their stability. The market plummets, credit freezes, and growth turns negative.

4. Europe Falls Apart

4. Europe Falls Apart

Europe seems to have avoided an all-out collapse of confidence in its ability to pay back its debt. But things can change, and fast fast. Indeed, the Greek debt crisis went from ignorable wire stories to front page news in a matter of days.

Here's the scenario. Slow growth in weak Eurozone states like Greece, Spain, and Italy turns negative and spooks investors, who demand higher returns on government debt. Europe's bond rates spike. Countries announce further austerity -- tax increases and spending cuts -- which strangles our biggest export market. The EU central bank responds by announcing a plan to write down troubled debt, which dings some Americans banks.

In a flight to quality debt, the dollar appreciates. This hurts our exports even more. As the trade deficit gapes open and manufacturing's good run dead ends, the stock market plummets, taking household wealth down with it. Families looking to restore balance sheets cut back on spending, and the American producer loses the American consumer and the European buyer. Growth turns negative.

5. Debt Finally Catches Up To Us

5. Debt Finally Catches Up To Us

Interest rates on U.S. debt are low today for one big reason. Investors trust the United States, at least more than they trust other countries. If the people giving us money suddenly have as little faith in America as Americans, that could change, and quickly.

Here's the scenario. The IMF recently said the United States has a 25 percent chance of seeing dramatically higher interest rates in the near future. But the bond market can strike without warning, as it did in Europe earlier this year. If uncertainty with our political process gets reflected in our interest rate, we'll have a harder time affording debt, 55% of which has to be rolled over in the next three years. Pension and mutual funds with government debt would be written down, causing Americans to save even more of their paychecks. We'd be left with two bad choices: tax cuts to juice consumption or tax hikes to please our lenders. But at that point, it would be too late to avoid a double dip.

FREE trial - Get out of Debt with DebtGoal Huge Coupon Savings!

Huge Coupon Savings!

$15 off orders of $40 or more at Botanic Choice. Free Shipping on $50 or more. Coupon Code BC15. Expires 9/30/2010

.

By Derek Thompson and Daniel Indiviglio

The Atlantic

It's been a brutal summer for the economy. The housing sector, like a balloon batted in the air one last time by the government credit, resumed its inevitable fall. Economic growth slowed to a lead-footed 1.6 percent, and job growth is even more anemic. Meanwhile, consumers arecranky, the trade gap is gaping.

Most signs point to a slow and steady recovery, but what if the pessimists are right, again? What if the United States isn't in the slow-lane to recovery, but rather on the precipice of another decline -- a double dip?

To see where this re-recession might begin, my colleague Dan Indiviglio and I imagined five financial earthquakes, each with a single epicenter: housing, consumers, toxic assets, Europe, and the debt. The following five scenarios are listed in order of likelihood.

1. Housing's Mini-Bubble PopsPerhaps nothing poses as a big of a concern to the U.S. economy as its housing market. It's unclear how the government's efforts to stabilize the market through a buyer credit, ultra-low mortgage rates, and mortgage modification programs will pan out. Did it just create another mini-bubble that's beginning to pop now that the support has been withdrawn?

Here's the scenario. Weak home sales and continuing foreclosures result in climbing real estate inventory. This has two effects. First, it makes new homes even less attractive which furtherreduces construction jobs. Second, it puts downward pressure on home prices, which makes it harder for struggling homeowners to sell their home to avoid foreclosure and also keeps strategic default rates high, exacerbating the problem. Lower home values encourage Americans to save more and spend less, since their wealth is effectively reduced. The Dow drops and credit markets tighten even further, suffocating private investment just as homeowners bunker down and slash spending. Growth turns negative.

2. You Break the EconomyYou, the American consumer, are reloading savings after a debt-fueled decade. But as any general will tell you, when an entire squad reloads at once, it leaves everybody vulnerable. It's the same with the economy.

Here's the scenario. Consumer sentiment continues to fall slowly, and spending turns negative again. Small businesses hold off to replenish their inventories or add new workers. Wages and hours freeze, and unemployment takes a leap toward 10 percent in October. Congress is paralyzed, because it's only weeks away from the mid-terms. The stock market sees business revenue trending flat, joblessness rising and Congress doing nothing, and it sparks a 300-point sell-off. Americans frightful for their savings cut back spending even more the next month, and overall growth turns negative.

3. Toxic Assets ReturnIf you closely followed the bank bailout, then you know it wasn't originally billed as simply throwing money at the banks. Instead, the Treasury intended to purchase the toxic assets from banks, which were the source of investors' uncertainty concerning bank stability. But the Treasury couldn't figure out a way to do this quickly enough to make it effective. As a result, the banks were largely stuck with these bad assets. We just don't know how bad, yet.

Here's the scenario. The residential real estate market's problems continue. Even once foreclosures begin to decline, we see waves of defaults, as modification program participants re-default at rates of 30% to 50%. Commercial mortgage-backed securities continue to deteriorate, as some businesses struggle with weak consumer demand. Home and commercial real estate values keep declining, and so do the value of the assets that back them. Banks with exposure to these toxic securities see another round of losses, and investors question their stability. The market plummets, credit freezes, and growth turns negative.

4. Europe Falls ApartEurope seems to have avoided an all-out collapse of confidence in its ability to pay back its debt. But things can change, and fast fast. Indeed, the Greek debt crisis went from ignorable wire stories to front page news in a matter of days.

Here's the scenario. Slow growth in weak Eurozone states like Greece, Spain, and Italy turns negative and spooks investors, who demand higher returns on government debt. Europe's bond rates spike. Countries announce further austerity -- tax increases and spending cuts -- which strangles our biggest export market. The EU central bank responds by announcing a plan to write down troubled debt, which dings some Americans banks.

In a flight to quality debt, the dollar appreciates. This hurts our exports even more. As the trade deficit gapes open and manufacturing's good run dead ends, the stock market plummets, taking household wealth down with it. Families looking to restore balance sheets cut back on spending, and the American producer loses the American consumer and the European buyer. Growth turns negative.

5. Debt Finally Catches Up To UsInterest rates on U.S. debt are low today for one big reason. Investors trust the United States, at least more than they trust other countries. If the people giving us money suddenly have as little faith in America as Americans, that could change, and quickly.

Here's the scenario. The IMF recently said the United States has a 25 percent chance of seeing dramatically higher interest rates in the near future. But the bond market can strike without warning, as it did in Europe earlier this year. If uncertainty with our political process gets reflected in our interest rate, we'll have a harder time affording debt, 55% of which has to be rolled over in the next three years. Pension and mutual funds with government debt would be written down, causing Americans to save even more of their paychecks. We'd be left with two bad choices: tax cuts to juice consumption or tax hikes to please our lenders. But at that point, it would be too late to avoid a double dip.

Photo credits from top: kworth30 (Flickr); Wikipedia; Wikipedia; Wikipedia; infrogmation (Flickr)

Read Full ArticleFREE trial - Get out of Debt with DebtGoal

$15 off orders of $40 or more at Botanic Choice. Free Shipping on $50 or more. Coupon Code BC15. Expires 9/30/2010

Saturday, September 4, 2010

State-Owned Banks as a Way to Rebuild the Housing and Real Estate Markets

Bruce B. Cahan

Bruce B. CahanStanford University

The financial literacy of America has improved markedly, nearly to college level, as a result of the global recession that started in 2007. What about state-owned banks, is the time ripe to explore that part of economic history?

Americans, now economists, can fill a green chalkboard from left to right, with the familiar logic of our situation:

- our housing bubble, pumped up by loose underwriting and shadow finance, burst,

- this caused Americans' perceived real estate wealth to evaporate,

- consumers reduced spending,

- lacking demand, companies reduced employment, profitability and investments,

- the economic uncertainty increased the volatility of the stock markets,

- this caused investors to flood into the bond markets, pushing interest rates to low levels, near zero, (aided by Federal Reserve monetary policy interventions),

- all of which now threatens a cycle or syndrome of deflation and recession.

Related Article:

FREE trial - Get out of Debt with DebtGoal

$15 off orders of $40 or more at Botanic Choice. Free Shipping on $50 or more. Coupon Code BC15. Expires 9/30/2010

Wednesday, August 25, 2010

Axing the Bankers’ Money Tree: Homeowners' Rebellion against Wall Street Recent Rulings Could Shield 62 Million Homes from Foreclosure

By Ellen Brown | |

URL of this article: www.globalresearch.ca/index. | |

Global Research, August 19, 2010 | |

webofdebt.com - 2010-08-18 | |

Over 62 million mortgages are now held in the name of MERS, an electronic recording system devised by and for the convenience of the mortgage industry. A California bankruptcy court, following landmark cases in other jurisdictions, recently held that this electronic shortcut breaks the chain of title, voiding foreclosure. The logical result could be 62 million homes that are foreclosure-proof. In a Newsweek article a year ago called "Too Big to Jail: Why Prosecutors Won’t Hit Wall Street Hard in the Subprime Scandal," Michael Hirsch wrote that we were unlikely to see trials and convictions like those in the savings and loan scandals of the 1980s, because fraud and blame have been so widespread that there is no one to single out and jail. Said Hirsch: “The sad irony is that in pleading collective guilt, most of Wall Street will escape whipping for a scheme that makes Bernie Madoff's shenanigans look like pickpocketing. At the crest of the real-estate bubble, fraud was systemic and Wall Street had essentially gone into the loan-sharking business.” “Unfortunately,” he added, “prosecution of fraud is the only way you're going to get reform on Wall Street.” Sure enough, a year later we got a banking reform bill that was so watered down that Wall Street got nearly everything it wanted. The too-big-to-fails, rather than being whittled down to size, have grown even bigger, circumventing antitrust laws; and they are being allowed to carry on pretty much as before. The Federal Reserve, rather than being called on the carpet, has been given even more power; and the Consumer Protection Agency -- the main part of the bill with teeth – has been put under the Fed’s watchful eye. Congress and the Justice Department seem to have bowed out, leaving no one to hold the finance industry to account. But the best laid plans even of Wall Street can sometimes go awry. In an ironic twist, the industry may wind up tripping over its own Achilles heel, the Mortgage Electronic Registration Systems or MERS. An online computer software program for tracking mortgage ownership and rights, MERS is, according to its website, “an innovative process that simplifies the way mortgage ownership and servicing rights are originated, sold and tracked. Created by the real estate finance industry, MERS eliminates the need to prepare and record assignments when trading residential and commercial mortgage loans.” Or as Karl Denninger puts it, “MERS own website claims that it exists for the purpose of circumventing assignments and documenting ownership!” MERS was developed in the early 1990s by a number of financial entities, including Bank of America, Countrywide, Fannie Mae, and Freddie Mac, allegedly to allow consumers to pay less for mortgage loans. That did not actually happen, but what MERS did allow was the securitization and shuffling around of mortgages behind a veil of anonymity. The result was not only to cheat local governments out of their recording fees but to defeat the purpose of the recording laws, which was to guarantee purchasers clean title. Worse, MERS facilitated an explosion of predatory lending in which lenders could not be held to account because they could not be identified, either by the preyed-upon borrowers or by the investors seduced into buying bundles of worthless mortgages. As alleged in a Nevada class action called Lopez vs. Executive Trustee Services, et al.: “Before MERS, it would not have been possible for mortgages with no market value . . . to be sold at a profit or collateralized and sold as mortgage-backed securities. Before MERS, it would not have been possible for the Defendant banks and AIG to conceal from government regulators the extent of risk of financial losses those entities faced from the predatory origination of residential loans and the fraudulent re-sale and securitization of those otherwise non-marketable loans. Before MERS, the actual beneficiary of every Deed of Trust on every parcel in the United States and the State of Nevada could be readily ascertained by merely reviewing the public records at the local recorder’s office where documents reflecting any ownership interest in real property are kept. . . . “After MERS, . . . the servicing rights were transferred after the origination of the loan to an entity so large that communication with the servicer became difficult if not impossible. . . . The servicer was interested in only one thing – making a profit from the foreclosure of the borrower’s residence – so that the entire predatory cycle of fraudulent origination, resale, and securitization of yet another predatory loan could occur again. This is the legacy of MERS, and the entire scheme was predicated upon the fraudulent designation of MERS as the ‘beneficiary’ under millions of deeds of trust in Nevada and other states.” MERS now holds over 62 million mortgages in its name, including over half of all new U.S. residential mortgage loans. But courts are increasingly ruling that MERS is merely a nominee, without standing to foreclose on the collateral that makes up a major portion of the portfolios of some very large banks. It seems the banks claiming to be the real parties in interest may have short-circuited themselves out of the chain of title entitling them to the collateral. Technicality or Fatal Flaw? To foreclose on real property, the plaintiff must be able to produce a promissory note or assignment establishing title. Early cases focused on MERS’ inability to produce such a note, but most courts continued to consider the note a mere technicality and ignored it. Landmark newer opinions, however, stress that this defect is not just a procedural but a substantive failure, one that is fatal to the plaintiff’s case. The latest of these decisions came down in California on May 20, 2010, in a bankruptcy case called In re Walker, Case no. 10-21656-E–11. The court held that MERS could not foreclosebecause it was a mere nominee, and that as a result plaintiff Citibank could not collect on its claim. The judge opined: “Since no evidence of MERS’ ownership of the underlying note has been offered, and other courts have concluded that MERS does not own the underlying notes, this court is convinced that MERS had no interest it could transfer to Citibank. Since MERS did not own the underlying note, it could not transfer the beneficial interest of the Deed of Trust to another. Any attempt to transfer the beneficial interest of a trust deed without ownership of the underlying note is void under California law.” In support, the judge cited In Re Vargas (California Bankruptcy Court); Landmark v. Kesler(Kansas Supreme Court); LaSalle Bank v. Lamy (a New York case); and In Re Foreclosure Cases (the “Boyko” decision from Ohio Federal Court). (For more on these earlier cases, seehere, here and here.) The court concluded: “Since the claimant, Citibank, has not established that it is the owner of the promissory note secured by the trust deed, Citibank is unable to assert a claim for payment in this case.” The broad impact the case could have on California foreclosures is suggested by attorney Jeff Barnes, who writes: “This opinion . . . serves as a legal basis to challenge any foreclosure in California based on a MERS assignment; to seek to void any MERS assignment of the Deed of Trust or the note to a third party for purposes of foreclosure; and should be sufficient for a borrower to not only obtain a TRO [temporary restraining order] against a Trustee’s Sale, but also a Preliminary Injunction barring any sale pending any litigation filed by the borrower challenging a foreclosure based on a MERS assignment.” While not binding on courts in other jurisdictions, the ruling could serve as persuasive precedent there as well, because the court cited non-bankruptcy cases related to the lack of authority of MERS, and because the opinion is consistent with prior rulings in Idaho and Nevada Bankruptcy courts on the same issue. RICO and Fraud Charges Other suits go beyond merely challenging title to alleging criminal activity. On July 26, 2010, a class action was filed in Florida seeking relief against MERS and an associated legal firm for racketeering and mail fraud. It alleges that the defendants used “the artifice of MERS to sabotage the judicial process to the detriment of borrowers;” that “to perpetuate the scheme, MERS was and is used in a way so that the average consumer, or even legal professional, can never determine who or what was or is ultimately receiving the benefits of any mortgage payments;” that the scheme depended on “the MERS artifice and the ability to generate any necessary ‘assignment’ which flowed from it;” and that “by engaging in a pattern of racketeering activity, specifically ‘mail or wire fraud,’ the Defendants . . . participated in a criminal enterprise affecting interstate commerce.” Local governments deprived of filing fees may also be getting into the act, at least through representatives suing on their behalf. Qui tam actions allow for a private party or “whistle blower” to bring suit on behalf of the government for a past or present fraud on it. In State of California ex rel. Barrett R. Bates, filed May 10, 2010, the plaintiff qui tam sued on behalf of a long list of local governments in California against MERS and a number of lenders, including Bank of America, JPMorgan Chase and Wells Fargo, for “wrongfully bypass[ing] the counties’ recording requirements; divest[ing] the borrowers of the right to know who owned the promissory note . . .; and record[ing] false documents to initiate and pursue non-judicial foreclosures, and to otherwise decrease or avoid payment of fees to the Counties and the Cities where the real estate is located.” The complaint notes that “MERS claims to have ‘saved’ at least $2.4 billion dollars in recording costs,” meaning it has helped avoid billions of dollars in fees otherwise accruing to local governments. The plaintiff sues for treble damages for all recording fees not paid during the past ten years, and for civil penalties of between $5,000 and $10,000 for each unpaid or underpaid recording fee and each false document recorded during that period, potentially a hefty sum. Similar suits have been filed by the same plaintiff qui tam in Nevada and Tennessee. Axing the Bankers’ Money Tree Most courts continue to look the other way on MERS’ lack of standing to sue, but the argument has picked up enough steam to consider the rather stunning implications. If MERS is not the title holder of properties held in its name, the chain of title has been broken, andno one may have standing to sue. In MERS v. Nebaska Department of Banking and Finance, MERS insisted that it had no actionable interest in title, and the court agreed. An August 2010 article in Mother Jones titled “Fannie and Freddie’s Foreclosure Barons” exposes a widespread practice of “foreclosure mills” in backdating assignments after foreclosures have been filed. Not only is this perjury, a prosecutable offense, but if MERS was never the title holder, there is nothing to assign. The defaulting homeowners could wind up with free and clear title. In Florida, Jacksonville Area Legal Aid attorney April Charney has been using the missing-note argument ever since she first identified that weakness in the lenders’ case in 2004. Five years later, she says, some of those homeowners are still in their homes. According to aHuffington Post article titled “‘Produce the Note’ Movement Helps Stall Foreclosures”: “Because of the missing ownership documentation, Charney is now starting to file quiet title actions, hoping to get her homeowner clients full title to their homes (a quiet title action ‘quiets’ all other claims). Charney says she’s helped thousands of homeowners delay or prevent foreclosure, and trained thousands of lawyers across the country on how to protect homeowners and battle in court.” If courts overwhelmed with foreclosures decide to take up the cause, the result could be millions of struggling homeowners with the banks off their backs, and millions of homes no longer on the books of some too-big-to-fail banks. Without those assets, the banks could again be looking at bankruptcy. As was pointed out in a San Francisco Chronicle article by attorney Sean Olender following the October 2007 Boyko decision: “The ticking time bomb in the U.S. banking system is not resetting subprime mortgage rates. The real problem is the contractual ability of investors in mortgage bonds to require banks to buy back the loans at face value if there was fraud in the origination process. “. . . The loans at issue dwarf the capital available at the largest U.S. banks combined, and investor lawsuits would raise stunning liability sufficient to cause even the largest U.S. banks to fail . . . .” Nationalization of these giant banks might be the next logical step – a step that some commentators said should have been taken in the first place. When the banking system ofSweden collapsed following a housing bubble in the 1990s, nationalization of the banks worked out very well for that country. The Swedish banks were largely privatized again when they got back on their feet, but it might be a good idea to keep some banks as publicly-owned entities, on the model of theCommonwealth Bank of Australia. For most of the 20th century it served as a “people’s bank,” making low interest loans to consumers and businesses through branches all over the country. With the strengthened position of Wall Street following the 2008 bailout and the tepid 2010 banking reform bill, the U.S. is far from nationalizing its mega-banks now. But a committed homeowner movement to tear off the predatory mask called MERS could yet turn the tide. While courts are not likely to let 62 million homeowners off scot free, the defect in title created by MERS could give them significant new leverage at the bargaining table. Ellen Brown developed her research skills as an attorney practicing civil litigation in Los Angeles. In Web of Debt, her latest of eleven books, she turns those skills to an analysis of the Federal Reserve and “the money trust.” She shows how this private cartel has usurped the power to create money from the people themselves, and how we the people can get it back. Her websites are www.webofdebt.com, www. READ ELLEN BROWN The Global Economic Crisis | |

Web of Debt: The Shocking Truth About Our Money System and How We Can Break Free Please support Global Research Global Research relies on the financial support of its readers. Your endorsement is greatly appreciated | |

| Subscribe to the Global Research e-newsletter | |

Disclaimer: The views expressed in this article are the sole responsibility of the author and do not necessarily reflect those of the Centre for Research on Globalization. The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible or liable for any inaccurate or incorrect statements contained in this article. To become a Member of Global Research The CRG grants permission to cross-post original Global Research articles on community internet sites as long as the text & title are not modified. The source and the author's copyright must be displayed. For publication of Global Research articles in print or other forms including commercial internet sites, contact: crgeditor@yahoo.com www.globalresearch.ca contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of "fair use" in an effort to advance a better understanding of political, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than "fair use" you must request permission from the copyright owner. For media inquiries: crgeditor@yahoo.com © Copyright Ellen Brown, webofdebt.com, 2010 The url address of this article is: www.globalresearch.ca/index. | |

© Copyright 2005-2007 GlobalResearch.ca Web site engine by Polygraphx Multimedia © Copyright 2005-2007 | |

Subscribe to:

Posts (Atom)